Key Takeaways

- HSTPA (2019) permanently eliminated vacancy decontrol, high-income deregulation, and the 20% vacancy bonus — rent-stabilized units can no longer exit the system

- Individual Apartment Improvements (IAIs) are now capped at $30,000 over 15 years (Tier 1) or $50,000 (Tier 2), down from unlimited

- Major Capital Improvements (MCIs) now expire after 30 years and are capped at 2% per year, down from 6% permanent increases

- Security deposits are limited to 1 month, late fees to $50 or 5% (whichever is less), and application fees to $20

- Preferential rent is now locked — if you charged below legal rent, that lower amount is the new base for increases

What Was HSTPA?

The Housing Stability and Tenant Protection Act of 2019 (HSTPA) was the most sweeping change to New York’s rent regulation system in 50 years. Signed into law on June 14, 2019, it eliminated virtually every mechanism landlords had used to increase rents beyond annual guidelines, exit the rent stabilization system, or recover capital investment costs.

HSTPA was not a minor adjustment. It was a fundamental restructuring of the economic framework for rent-stabilized housing in New York. Before HSTPA, rent stabilization was a system that units could eventually exit through vacancy decontrol or high-income deregulation. After HSTPA, rent stabilization is permanent.

If you own rent-stabilized property in New York, everything that follows is the law you operate under today. There is no sunset date. There is no legislative effort with realistic prospects of repeal. This is the permanent framework.

The Complete Before-and-After

Vacancy Bonus

| Feature | Before HSTPA | After HSTPA |

|---|---|---|

| Vacancy increase | 20% automatic increase when a unit became vacant (longevity bonuses also applied: 0.6% per year of prior tenancy for 1-year leases, 1.2% for 2-year leases) | Eliminated entirely. No vacancy increase of any kind. The legal regulated rent carries over to the next tenant at the same amount. |

Impact: Before HSTPA, a landlord with a unit renting at $1,500 could set the new tenant’s rent at $1,800 (20% vacancy bonus) plus longevity bonuses. Now, the new tenant’s starting rent is $1,500 plus only the current RGB guideline increase. Over multiple turnovers, this eliminates the primary mechanism landlords used to bring stabilized rents closer to market rates.

Vacancy Decontrol

| Feature | Before HSTPA | After HSTPA |

|---|---|---|

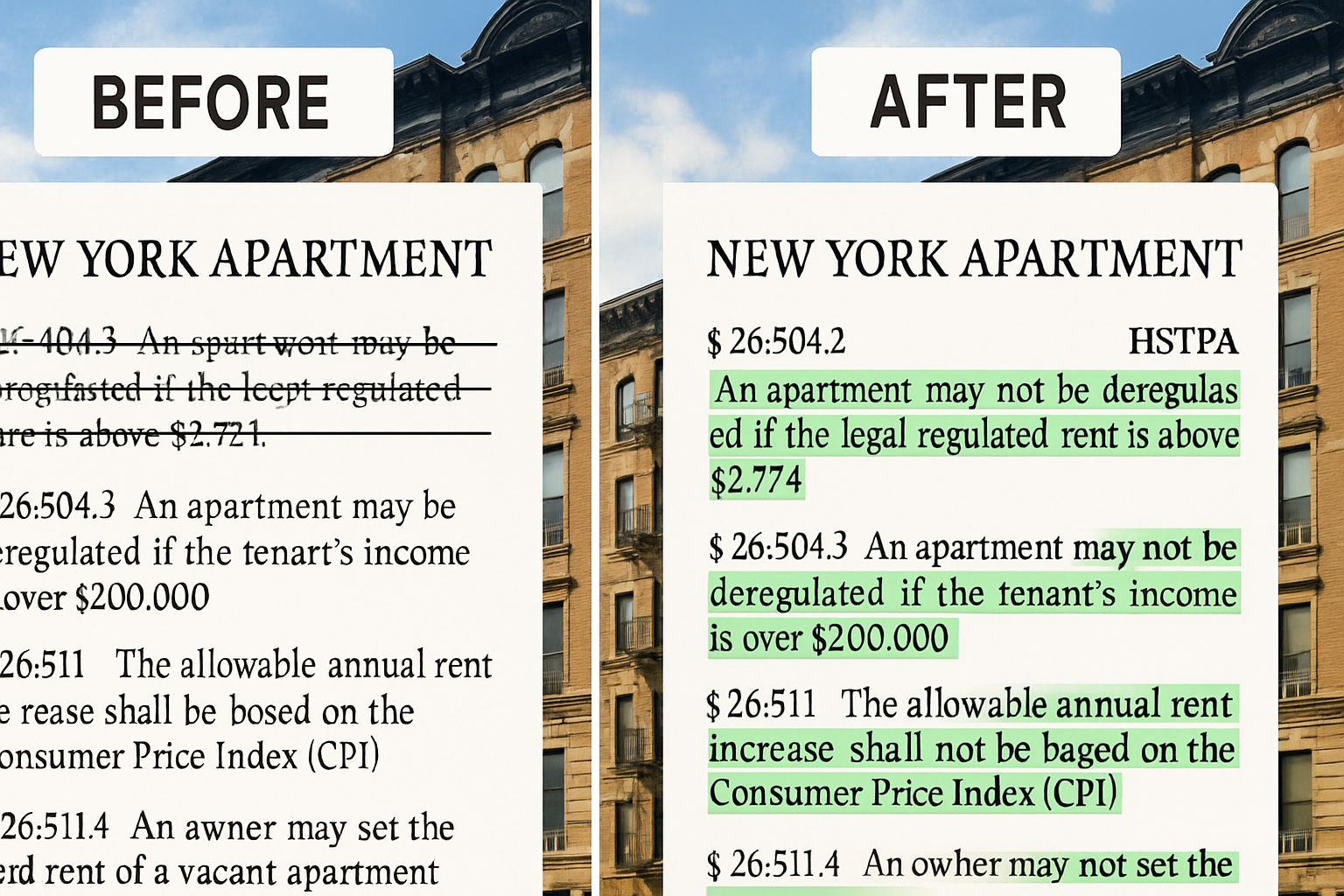

| Deregulation threshold | When legal rent reached $2,774.76 (adjusted periodically) and the unit became vacant, the unit exited rent stabilization permanently | Eliminated entirely. No unit can exit rent stabilization based on rent level, regardless of how high the legal rent becomes. |

Impact: This was the biggest structural change. Before HSTPA, the rent-stabilized stock was shrinking by an estimated 25,000-30,000 units per year as high-rent units became vacant and deregulated. After HSTPA, the stock is essentially permanent. A unit that is rent-stabilized today will be rent-stabilized in perpetuity.

High-Income Deregulation (Luxury Decontrol)

| Feature | Before HSTPA | After HSTPA |

|---|---|---|

| Income-based deregulation | Landlord could petition to deregulate a unit if household income exceeded $200,000 for two consecutive years AND the rent was above the deregulation threshold | Eliminated entirely. No deregulation based on tenant income, regardless of how much the tenant earns. |

Impact: High-income deregulation was used sparingly (it required the landlord to know or discover the tenant’s income), but it was a path to deregulation. It is now gone. A tenant earning $500,000 per year in a rent-stabilized apartment paying $1,200 per month retains full rent stabilization protections.

Preferential Rent

| Feature | Before HSTPA | After HSTPA |

|---|---|---|

| Preferential rent treatment | If a landlord charged below the legal regulated rent (a “preferential” rent), the landlord could revoke the preference at any lease renewal and charge up to the full legal rent | Locked in. The preferential rent becomes the base for all future RGB increases. The landlord can only increase from the preferential rent, not from the legal regulated rent. |

Impact: Before HSTPA, landlords offered preferential rents to attract tenants in slow markets, knowing they could jump to the legal rent later. Now, that strategy backfires. If you offered a preferential rent of $1,200 on a unit with a legal rent of $1,800, your future increases are calculated on $1,200, not $1,800. The $600 gap is permanently lost.

Exception: Preferential rents may still be reverted to legal rent when the apartment is vacated and a new tenant moves in. The lock-in applies during the tenancy, not across tenancies.

Individual Apartment Improvements (IAIs)

| Feature | Before HSTPA | After HSTPA |

|---|---|---|

| Spending cap | $15,000 with no time limit — could spend $15K per vacancy indefinitely, each time adding a permanent rent increase | Tier 1: $30,000 over a rolling 15-year period Tier 2: $50,000 over 15 years (for tenancies of 25+ years or vacancies between June 14, 2022 and June 15, 2024) |

| Rent increase calculation | 1/40th of improvement cost (buildings with 35+ units) or 1/60th (under 35 units) added permanently to rent | 1/168th (35+ units) or 1/180th (under 35 units) added to rent for 15 years only, then the increase expires |

| Duration | Permanent | 15 years — the IAI increase is removed from the legal rent after 15 years |

Impact: IAIs were the primary tool for increasing rents on stabilized units. Before HSTPA, a $15,000 kitchen renovation on a unit in a building with fewer than 35 units would add $250/month permanently (1/60th). After HSTPA, a $25,000 kitchen renovation adds $138.89/month (1/180th) for 15 years, then drops off. The economics of renovation have fundamentally changed. See our detailed guide on MCI and IAI Caps After HSTPA.

Major Capital Improvements (MCIs)

| Feature | Before HSTPA | After HSTPA |

|---|---|---|

| Annual cap on tenant’s rent increase | 6% of tenant’s rent per year | 2% of tenant’s rent per year |

| Duration | Permanent — MCI increases were added to legal rent indefinitely | 30 years — MCI increases expire and are removed from legal rent after 30 years |

| Phase-in period | MCI increases could be collected at up to 6% of rent annually until the full increase was applied | Capped at 2% of rent annually, extending the phase-in period significantly |

Impact: MCIs remain available, but the economic return is dramatically reduced. A $500,000 boiler replacement in a 50-unit building previously generated a permanent rent increase phased in at 6% per year per tenant. Now, the same improvement generates a temporary increase (30-year expiration) phased in at only 2% per year. For many buildings, the MCI rent increase no longer covers the financing cost of the improvement.

Security Deposits

| Feature | Before HSTPA | After HSTPA |

|---|---|---|

| Maximum deposit | No statutory limit (typically 1-2 months; some landlords collected 2-3 months) | 1 month’s rent maximum. No additional deposits (pet deposits, last month’s rent, key deposits) are permitted. |

| Interest | Required for buildings with 6+ units | Required for buildings with 6+ units (unchanged) |

| Return timeline | Reasonable time | 14 days with itemized statement of deductions |

For the complete guide on security deposit rules, see our article on NYC Security Deposits, Late Fees, and Application Fees.

Late Fees

| Feature | Before HSTPA | After HSTPA |

|---|---|---|

| Maximum late fee | No statutory cap (lease-defined; some landlords charged 5-10% with no cap) | $50 or 5% of monthly rent, whichever is LESS. Cannot be charged until rent is at least 5 days late. |

Application Fees

| Feature | Before HSTPA | After HSTPA |

|---|---|---|

| Maximum fee | No statutory cap (landlords commonly charged $50-$150+) | $20 maximum. This must cover the actual cost of a background check and/or credit check. No additional charges for applications. |

Rent Overcharge Claims

| Feature | Before HSTPA | After HSTPA |

|---|---|---|

| Lookback period | 4 years — only rent history within the prior 4 years could be examined to determine overcharges | 6 years — the lookback period for overcharge claims is now 6 years. Additionally, DHCR can examine the full rent history (beyond 6 years) if there is evidence of fraud. |

| Treble damages | Available only if the overcharge was willful | Available if the overcharge was willful (same standard, but the longer lookback period increases exposure) |

Lease Renewal Notice

| Feature | Before HSTPA | After HSTPA |

|---|---|---|

| Landlord notice to tenant | 90-150 days before lease expiration | 90-150 days before lease expiration (unchanged) |

| Tenant response time | 60 days from notice | 60 days from notice (unchanged) |

| Late notice penalty | Tenant could remain on same terms if landlord failed to provide timely notice | Same — but HSTPA strengthened the tenant’s position by eliminating the landlord’s ability to discontinue a preferential rent at renewal |

What Landlords Lost — The Summary

Here is the complete list of mechanisms that HSTPA eliminated or restricted, and the revenue impact:

| Mechanism | Status | Revenue Impact |

|---|---|---|

| 20% vacancy bonus | Eliminated | Loss of ~$300-600/month per turnover on typical unit |

| Vacancy decontrol ($2,774) | Eliminated | Units permanently locked in stabilization |

| High-income deregulation ($200K) | Eliminated | No path to market-rate conversion |

| Preferential rent revocation | Locked | Gap between preferential and legal rent permanently lost |

| Unlimited IAI spending | Capped ($30K-$50K/15yr) | ~60-70% reduction in per-unit renovation ROI |

| Permanent IAI increases | 15-year expiration | IAI increases are temporary, not permanent |

| 6% MCI phase-in | Reduced to 2% | Slower cost recovery, reduced incentive for building improvements |

| Permanent MCI increases | 30-year expiration | MCI increases eventually expire |

| 2+ month security deposits | Capped at 1 month | Reduced security against damage/nonpayment |

| Unregulated late fees | Capped at $50/5% | Minimal revenue impact, but reduced leverage |

| Unregulated application fees | Capped at $20 | Cannot recover full screening costs |

What Landlords Can Still Do

HSTPA restricted many tools, but it did not eliminate all avenues for increasing rental income or managing stabilized properties effectively:

- RGB annual increases: You can still apply the annual RGB guideline increase to every lease renewal. In years like 2024-2025 (3.0% for 1-year leases), this provides real revenue growth. In freeze years like 2026-2027, it does not.

- IAIs within the caps: You can still invest up to $30,000 (or $50,000 Tier 2) per unit over 15 years and add the calculated increase to rent for 15 years. Strategic renovations that maximize the IAI benefit are still worthwhile.

- MCIs: Building-wide improvements still qualify for MCI increases, albeit capped at 2% per year with a 30-year expiration.

- Hardship applications: If your building is genuinely operating at a loss, you can file a hardship application with HCR for above-guideline increases.

- Market-rate rent on new tenancies (with no vacancy bonus): While you cannot add a vacancy bonus, you can charge the legal regulated rent (with the current RGB increase) to a new tenant. The key is that the legal rent is now lower than it would have been under the old system.

“HSTPA did not just change the rules — it changed the entire business model for rent-stabilized housing. Before 2019, landlords could plan for eventual deregulation and use vacancy bonuses to approach market rents over time. That model is gone. The landlords who have adapted are the ones who treat stabilized housing as a permanent, long-term-hold asset class with different return expectations.”

— Rachid Abadli, Founder & CEO at LeaseBase

Frequently Asked Questions

Can HSTPA be repealed?

Theoretically, yes — any law can be amended or repealed by the legislature. Practically, repeal is extremely unlikely. HSTPA passed with strong legislative support, tenant advocacy organizations are well-organized, and there is no significant political movement to roll it back. Landlords should plan as if HSTPA is permanent.

Are there any legal challenges to HSTPA?

Several legal challenges have been filed, primarily arguing that HSTPA’s restrictions constitute an unconstitutional taking of property without just compensation. As of mid-2026, no court has struck down HSTPA or any of its provisions. Federal courts, including the Second Circuit Court of Appeals, have upheld the law’s constitutionality.

Does HSTPA apply to rent-controlled apartments?

HSTPA primarily addresses rent stabilization, not the older rent control system. Rent-controlled apartments (pre-1947 buildings where the tenant has continuously resided since before July 1, 1971) have their own rules set by the Maximum Base Rent system. However, HSTPA’s security deposit, late fee, and application fee limits apply to all residential rentals, including rent-controlled units.

Can I still charge a preferential rent to a new tenant?

Yes. You can offer a preferential rent below the legal regulated rent. However, understand that the preferential rent becomes the base for future RGB increases during that tenancy. When the tenant leaves and a new tenant moves in, you can set the rent at the legal regulated rent (not the preferential rent). But the legal rent itself will be lower than it would have been under the old system because of the locked-in preferential rent during the prior tenancy.

What happens to IAI increases after 15 years?

The IAI portion of the legal regulated rent is removed. If a unit’s legal rent is $1,800, of which $150 is from an IAI, the legal rent drops to $1,650 when the 15-year period expires. However, any RGB guideline increases that were applied on top of the IAI amount during those 15 years are also partially reduced, creating a compounding reduction.

Does HSTPA affect buildings outside NYC?

Yes. HSTPA applies to all rent-stabilized units in New York State, including those in ETPA municipalities in Nassau, Westchester, Rockland, and Ulster counties. The security deposit ($1 month max), late fee ($50/5%), and application fee ($20) limits apply to all residential rentals statewide, regardless of stabilization status.

Navigate HSTPA Compliance With Confidence

HSTPA’s changes are complex, but they are knowable. The landlords who struggle are the ones who don’t track their legal rents accurately, miss IAI or MCI expiration dates, or fail to account for preferential rent lockdowns in their financial planning.

LeaseBase’s NYC Rent Stabilization Calculator tracks every component of your legal rent — RGB increases, IAI additions and expirations, MCI phase-ins and expirations, and preferential rent calculations. You always know your exact legal rent, your maximum allowable increase, and when any temporary increases are scheduled to drop off.

Related Reading

- NYC Rent Freeze 2026-27: What the 0% RGB Increase Means

- MCI and IAI Caps After HSTPA

- New York Good Cause Eviction Law: The Complete Guide

- Rent Stabilization vs Good Cause Eviction: Which Law Applies?

- Is Your NY Rental Exempt from Good Cause?

- NYC Security Deposits, Late Fees, and Application Fees

- Good Cause Eviction Opt-In Tracker